Cleaner vehicles and better monitoring: New RDE regulations on light-duty vehicles in India

White paper

Costs and CO2 emissions reduction benefits of potential phase 3 fuel consumption standards for India’s passenger vehicles

India has a national goal of 30% battery electric vehicle (BEV) sales by 2030, and this study evaluates how prospective phase 3 fuel consumption standards for the passenger car segment could help meet the 30% target. The authors evaluate CO2-reducing internal combustion engine vehicle (ICEV) technologies and compare the direct manufacturing costs (DMCs) of BEVs with the DMCs of improved ICEVs for a variety of vehicle classes. Two compliance strategies are examined. In one, ICEV technology is used until no further reduction in CO2 emissions is possible and the reduction limit for a new CO2 emission level can only be met with a significant shift in production to BEVs. In the second, the shift from ICEV to BEV is earlier and happens at an optimal transition point that minimizes compliance costs.

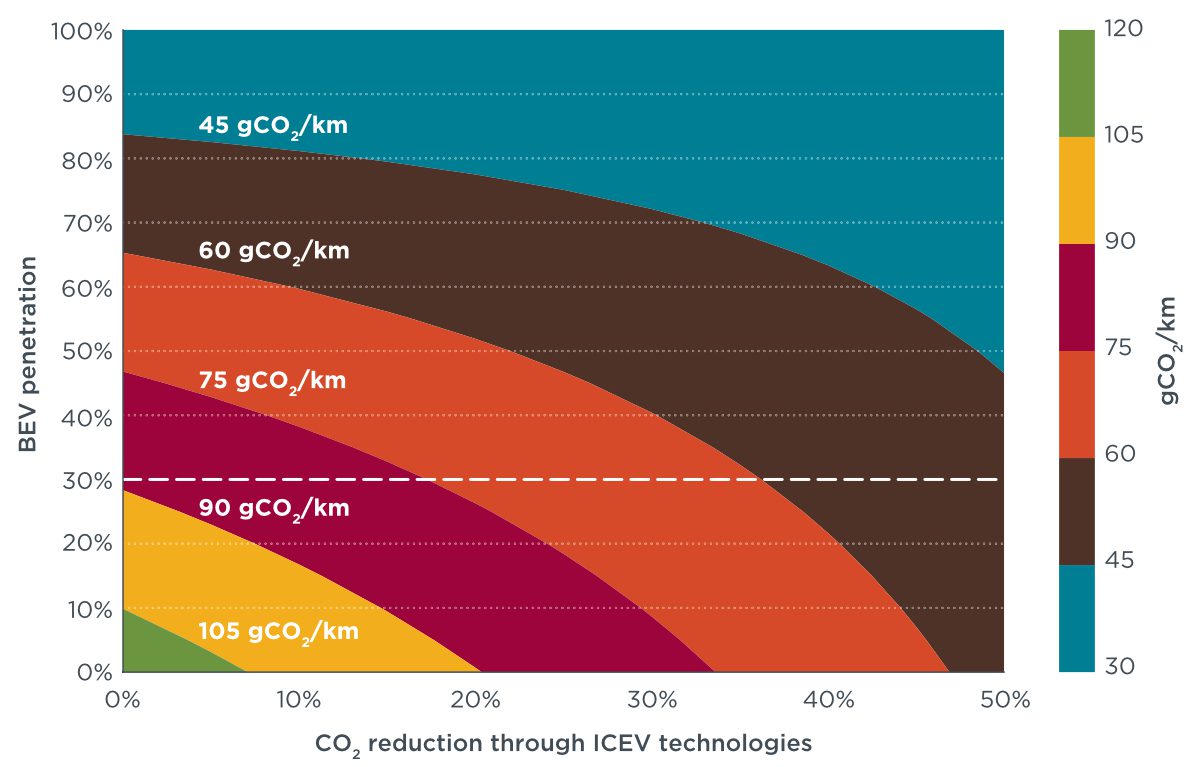

The figure below shows the potential fleet-average CO2 emission standards for passenger cars using various CO2-reducing technology and BEV sales percentages. There are no super credits assigned to BEVs; the sales of BEVs are absolute numbers. As illustrated, 30% BEV penetration is possible at a fleet-average target of 90 gCO2/ km. This implies manufacturers could meet this standard solely by adopting 30% BEVs in their fleets and zero ICEV improvement on the other end.

Figure. Possible passenger car fleet-average CO2 emission standards for India, in gCO2/km, that could be achieved through improved ICEV technologies and/or BEVs with no super credits.

Although super credits are helpful in incentivizing BEVs, their use inflates the actual number of BEVs sold, and manufacturers do not need to reduce the ICEV CO2 emissions as much as they would have to without super credits. This is because the super credits allow them to meet fleet-average CO2 targets with a relatively small number of BEVs. Given that the real-world CO2 emissions of ICEVs are about 1.4 times higher than New European Driving Cycle type-approval values, the fleet-average real-world CO2 emissions of India’s fleet would be expected to be significantly higher than the standard suggests with the use of super credits. An effective way to prevent this would be to launch phase 3 targets earlier, in 2027, and then gradually reduce the super credits by 1 until they are phased out in 2030.